Happiness for everyone: SoftBank's too-connected-to-fail strategy

The company is betting that networks beat markets

SoftBank has always had a knack for placing heroic bets on long-term trends that bind technology to consumers. After all, this is the company that unabashedly says “our mission is to harness the raw, unlimited power of the Information Revolution and channel it in a direction that makes people happier”.

After years of gains from early internet winners like Yahoo and Alibaba, a pivot to telecoms, semiconductors and ridesharing, SoftBank has been on a tear since 2025, riding a wave of well-timed investments in OpenAI and the broader AI infrastructure ecosystem. At the beginning of June 2026, thanks to a more than 200% share price rise over the past year, SoftBank Group surpassed Toyota Motors in market capitalisation terms—something it hasn’t done since 2000.

There are two fascinating elements of SoftBank’s reincarnation that deserve more attention than they are getting. The first is the painstaking work that is required to track the company’s many investments and link them to the financing strategies that will be critical to realising the company’s race-to-scale strategy. The second, and less discussed element of SoftBank’s gravity-defying performance, is the bet that is being placed on Chairman and CEO Masayoshi Son’s ability to leverage his relationships with Donald Trump, Sam Altman, Japanese business and political leaders, and his key funders from the Middle East.

What stands out is that SoftBank is placing an old-fashioned wager that the AI assets they have accumulated plus the relationships that Masayoshi Son has cultivated, ensure that the company survives any political or financial repercussions if parts of the story come unstuck. Like SpaceX, SoftBank is a mega-cap with an over-cooked valuation that will require a long list of things to go right at a time when global geopolitics can either support or destroy their dreams. This poses a major challenge for investors who can’t afford to ignore the stock.

SoftBank financial snapshot—a leveraged play on AI ecosystem lock-in

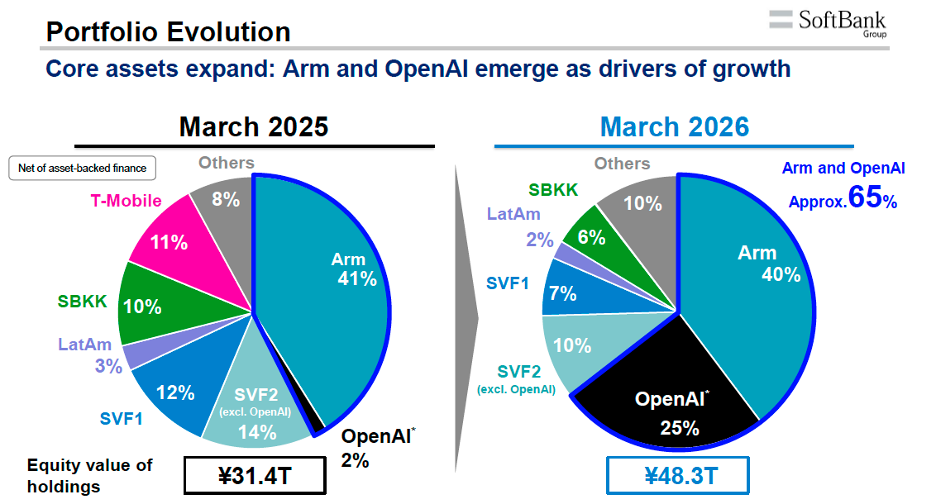

SoftBank’s financial fundamentals rest on its distinctive mix of direct holdings and indirect investments held by the SoftBank Vision Fund 2 (SVF2). These investments are then paired with active portfolio management and financing initiatives. This formula delivers operating cash flow in the good years and valuation gains that drive NAV appreciation, which is SoftBank’s key growth metric.

Source: SoftBank Group, FY 2025 Investor Briefing, May 13, 2026, https://group.SoftBank/en/news/webcast/20260513_03

In FY2025 ending in March 2026, the two key drivers for SoftBank’s resurgence were the US$64.6 billion investment in OpenAI and its controlling interest in ARM, the UK-based designer of highly efficient graphics processing units (GPUs) for mobile phones, that is now moving into a range of AI-related applications. The investment in OpenAI delivered a non-cash valuation gain of US$45 billion in FY2025 and now accounts for 25% of SoftBank’s NAV, while ARM’s contribution to the NAV grew by 50% to JPY15.9 trillion and also supported margin financing efforts.

SoftBank is all-in on the AI revolution, adopting a race-to-scale strategy as a platform provider using OpenAI and ARM technology inputs paired with big investments in data centres and power infrastructure in the US. Ambitious investments in enterprise AI solutions for Japan’s industrial leaders are also in the pipeline, driven by the hope that this AI infrastructure could shape key global supply chains. The goal is to ensure that SoftBank will be one of a small number of leaders capable of an AI ecosystem lock-in by owning the entire AI stack from hardware to semiconductors and data centres, as well as the model intelligence, agent orchestration and application layers.

If the tone of SoftBank’s May 2026 investor calls is any indication, financial analysts from the major firms are tracking the big dream but prefer to stay resolutely focused on the company’s financial engineering. This requires careful navigation of the investment and cash management trends that drive NAV and shape the company’s debt capacity.

Perhaps the most telling question from the session highlighted the fact that SoftBank’s strategic embrace of OpenAI may be delivering dramatic non-cash valuation gains but no cash, resulting in the lowest free cashflow yield seen for many years. This is a development that worries analysts and marks a departure from recent years where management used cash generative holdings like Alibaba to balance the variable cash flow profile of growth-stage holdings.

Analysts were also eager to get more information on the financial dimensions of related-party transactions with ARM and with OpenAI related to Cristal intelligence, the enterprise AI initiative. Here analysts went away with little to show for their efforts. Although just enough information was provided to estimate SoftBank’s rough contribution to ARM revenues, all they were offered on OpenAI was a “no comment”. The same was true when management was asked about funding arrangements for Energy Global, the vehicle that is investing in US energy projects as part of the Stargate AI infrastructure venture.

There’s no reason to think that analysts will abandon SoftBank because it remains the opaque conglomerate that it has always been. Buy recommendations still outnumber holds by a healthy margin. But there was little indication that management has all the tools that might be needed if AI valuations hit an air pocket and leading banks like Mizuho or JP Morgan that have backed their US$40 billion bridge loan arranged in March get anxious.

AI politics = friends + scale + speed

To keep its momentum bet alive, SoftBank is rushing to get even bigger. That makes the political and financial risks around their market development dreams something to monitor carefully. Softbank’s biggest funders will have to make a call on whether Masayoshi Son can marshal the political support SoftBank needs to win hard and soft forms of government support in both the United States and Japan.

And it is this geopolitical dimension that has largely gone unanalysed. It is somehow taken for granted that SoftBank has just the right political DNA needed to garner policy backing in both the US and in Japan, and that there is limited downside risk to the public showmanship of the Trump era.

It’s no secret that Masayoshi Son and Donald Trump have a mutually beneficial relationship. Just after Trump’s first election in 2016, Son traveled to Trump Tower and promised to invest US$50 billion in the US paired with a promise to create 50,000 jobs.

The postmortem on this investment strategy suggests that while it may have bought some goodwill, it didn’t deliver the promised outcomes or lead to a strategic breakthrough for SoftBank Group. Much of the capital that flowed into the US under the SoftBank banner came from SoftBank Vision Fund 1(SVF1), some of which went to notable flame outs like WeWork. An additional irony is that more than half of the capital in SVF1 came from Saudi funds.

Fast forward to December 2024, and Son traveled to meet the newly re-elected President Trump at Mar-a-Lago where he committed US$100 billion in new investments in the US to create 100,000 jobs. In a Trumpian bit of theatre, Trump pushed Son to agree to try to make it US$200 billion.

The 2024 promises have been followed by an active period of ambitious dealmaking for SoftBank in the US in addition to the well-timed portfolio investments in OpenAI stock. The vehicle for this deployment is SoftBank’s participation as financial lead for Stargate LLC, an AI infrastructure JV bringing together OpenAI, Oracle, and MGX—a Mubadala-backed UAE AI vehicle. Stargate, which is routinely described as a US$500 billion venture, has targeted seven sites for coordinated power and data centre development.

With a stated goal of delivering 9GW of power across seven sites, Stargate has a complex roadmap of regulatory and financial hurdles to navigate. Progress has been made, but tracking the net flow of capital will be challenging as deployment will be shared between SoftBank Group and SVF2. It’s also expected that project and asset-backed financing will play a role in jumpstarting these projects all of which have to navigate an increasingly hostile US political environment.

Despite the crosscurrents, SoftBank has stepped up yet again to make sure that it is keeping pace with the top-tier of Trump-aligned donors. In late May 2026, it was reported that SoftBank has committed US$50 million to Trump’s presidential library project, managed by his son Eric Trump. This makes SoftBank the largest donor to date and positions it ahead of Meta and Paramount, which is owned by the Oracle founder Larry Ellison.

It’s important to appreciate that Son’s political gestures in the US are not formally endorsed by the Japanese government. As a result, SoftBank’s investments enjoy only an ambiguous link to Japan’s US$550 billion US economic security deal.

Nonetheless, while SoftBank has been busy building political capital in the US, it has not been ignoring the need to stay in tune with Japanese policy goals. That is what makes SoftBank’s investment in Cristal intelligence in Japan important to track. A report from Nikkei Asia in late May 2026 suggests that roughly 30 leading Japanese industrial companies may be considering investments alongside SoftBank in a new Cristal-linked venture that will develop enterprise AI solutions tailored to Japanese companies. Early movers are said to include NEC, Honda Motor, and Sony Group with MUFG Group, SMBC, Mizuho Bank, Nippon Steel, and Kobe Steel also in the frame.

The outlines of this initiative could emerge soon if the venture wins backing from Japan’s New Energy and Industrial Technology Development Organization (NEDO). This would lock in government backing and establish SoftBank as the de facto national champion for physical AI in Japan.

What happens when connections + scale meet implementation risks?

It’s always challenging to predict how equity investors will respond to political risk, especially at a time when geopolitical pressures are reshuffling alliances and regulators are racing to define appropriate boundaries for privacy and security related to AI. The valuation technicians may simply opt to bump up discount rates on future cash flows while strategists start pumping out disruptive scenarios.

Either way, SoftBank’s public embrace of Trump and US-style AI dominance calls for more attention than it’s getting. American investors are deep into a period of cognitive dissonance on AI. In part, this is a byproduct of the political noise machine that is common to Trump administrations. No one wants the party to end, but AI is no longer a simple tech story. Trump loves to anoint winners who need his backing. That said, no one should expect him to be around to clean up the mess as he heads toward lame duck status, especially when some of the most ambitious US AI projects are riddled with implementation risk that the next generation of politicians will have to sort out.

Investors in SoftBank would do well to cast a more cynical eye over some of its aspirations, especially given the company’s weak governance fundamentals. Their AI race-to-scale strategy deserves more careful analysis. It’s hard to shake the feeling that this is yet another debt-fueled growth strategy that may ultimately require political and financial support from people other than Donald Trump.

US voters are no longer in love with data centres or higher power bills. What happens if Japan also pivots to a more carefully regulated version of AI with multiple players rather than ecosystem lock-in? Maybe it’s best that Masayoshi Son didn’t go to Trump’s UFC cage fight birthday party.

Copyright of Ninepin Limited, 2026