The China companies ditching Cayman for Hong Kong

There is no rush to leave the Caribbean but the issuers moving have a lot in common

Domicile may be the most neglected feature of Hong Kong's stock market. Investors obsess over earnings, dividends and valuations, but seldom ask where the company legally resides.

That indifference has had consequences. Corporate disputes involving Hong Kong-listed issuers frequently turn on Cayman and Bermuda statutes, leaving Hong Kong with a thriving stock exchange but a surprisingly thin body of shareholder case law.

By 2020, only 8% of companies listed in Hong Kong were incorporated there. The typical issuer had assets on the mainland, capital raised in the city and a holding company incorporated in the Cayman Islands or Bermuda.

The arrangement suited issuers, bankers and policymakers. Offshore structures gave companies access to foreign capital, an ability to retain funds outside mainland China and considerable flexibility over governance arrangements. Investors accepted offshore legal complexity as the price of access to Chinese growth.

Which is why it is worth taking a closer look at the cohort of listed companies now voluntarily leaving Cayman and Bermuda for Hong Kong’s legal orbit. The numbers are small, but the companies making the move are anything but random.

Nobody expected listed companies to read this

The vehicle for doing this is a dry tweak to Hong Kong company law that at first glance seemed to generate a flurry of client memoranda and little else.

The snappily-titled “inward re-domiciliation regime” invited companies to move their legal home to the city without going through the complex and costly process of having to wind up the company and re-incorporate. Introduced in May 2025, it was marketed to appeal to private companies, family offices and multinationals seeking a base in Hong Kong.

The first company to sign up was exactly the sort of entity policymakers had in mind: the overseas-incorporated private subsidiary of PetroChina Investment, looking to simplify its structure. By May 2026, 28 companies had migrated to Hong Kong under the scheme.

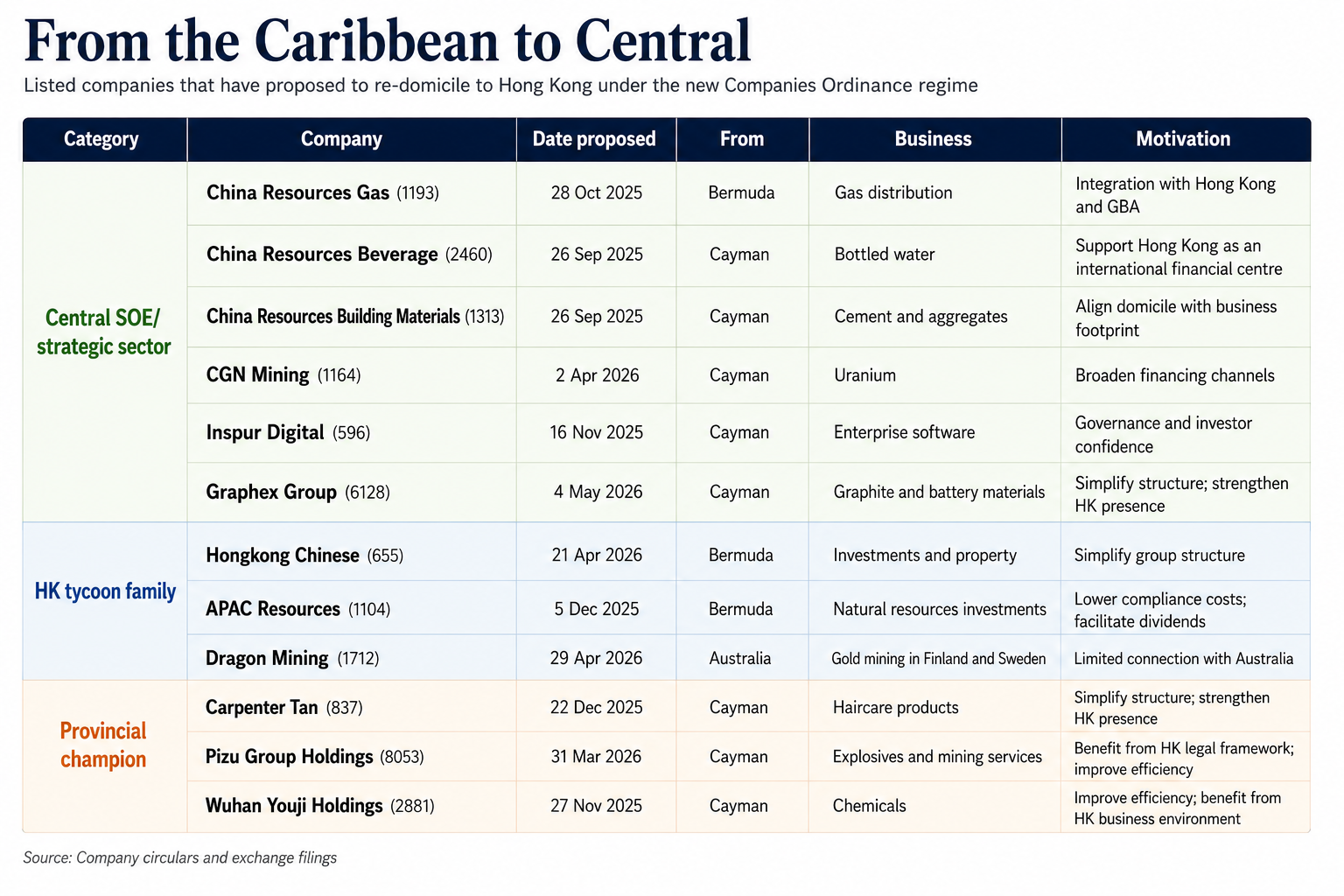

More surprising has been the take up among Hong Kong listed companies. The issuers below have announced plans to move their place of incorporation from Cayman or Bermuda to Hong Kong. While it is no exodus, the companies making the move are telling:

Three broad themes emerge. The early movers are disproportionately subsidiaries of central SOEs or companies operating in strategically important sectors, provincial private champions, and issuers associated with some of Hong Kong's oldest business families.

CGN Mining, Inspur Digital and Graphex are exposed to sectors Beijing regards as critical, while three others belong to the China Resources stable, one of China’s largest SOE conglomerates with deep roots in the state apparatus.

Hong Kong-listed CGN Mining is controlled by the broader CGN Group, one of China’s two dominant nuclear players (the SOE and some of its affiliates are on US export-control lists). The Hong Kong entity is described by CGN as the group’s only overseas uranium resource investment and trading platform.

Inspur Digital is part of the wider Inspur Group, ultimately controlled by the Shandong provincial government. Inspur occupies a key position in China’s efforts to build out its digital infrastructure, supplying servers, cloud infrastructure and data platforms to government agencies, SOEs and other public sector entities.

Graphex does not have obvious political connections, but operates in a sector considered strategically important: the processing of graphite and related materials essential for lithium-ion batteries.

Pizu Group operates in the tightly regulated civil explosives sector and likely enjoys strong provincial relationships, particularly in Inner Mongolia and Tibet. Wuhan Youji is essentially a listed subsidiary of the privately owned Linuo group and looks more like a provincial industrial heavyweight than a company with deep central government ties.

At the other end of the spectrum sit mature businesses such as APAC Resources and Dragon Mining, and Hongkong Chinese, both part of Hong Kong tycoon groups (Allied Group and Lippo respectively).

In framing the rationale for moving, most companies reached for the standard Hong Kong circular playbook, citing streamlined group structures, administrative efficiency and Hong Kong's rule of law. China Resources Gas was the notable exception, explicitly linking the move to the Greater Bay Area and China’s “dual circulation” development strategy.

Given who the early movers are, it is easy to imagine others of their ilk reaching the same conclusion. Companies with close ties to the Chinese state, exposure to strategically important industries or membership of Hong Kong's old tycoon families may increasingly find that Cayman and Bermuda no longer offer advantages worth preserving.

Leaving paradise

The sample is small. But if policymakers in Beijing and Hong Kong wanted companies to gradually unwind offshore structures, the first tranche would probably look much like this cohort.

Firefly previously argued that China wants not only its IPOs back, but the liquidity that comes with them. Since 2023 China’s securities regulator has streamlined approvals for H-share listings and repeatedly voiced support for Hong Kong as the preferred overseas listing venue for mainland companies. Reuters reported earlier this year that some red-chip companies had been nudged to unwind offshore structures before pursuing Hong Kong IPOs.

The IPO numbers suggest the CSRC is delivering. In 2020, only 12% of companies listing in Hong Kong were incorporated in the PRC. In the first half of 2026, the figure was close to 90%.

It may not amount to a concerted campaign against Cayman or Bermuda, but the direction of travel is hard to miss. If listings and liquidity are being repatriated, it is not inconceivable that policymakers might also prefer issuers themselves to reside within Hong Kong's legal framework.

The Cayman Islands can sleep easy

There is no sign of a rush for the exits, and Cayman’s grip on Hong Kong’s stock market remains formidable: nearly four out of five Hong Kong-listed companies were incorporated in Cayman or Bermuda in 2020, and shifting those numbers would require a substantial effort by issuers. Hundreds of boards would need to rewrite constitutional documents, convene meetings and persuade shareholders to approve special resolutions.

Companies are not known for moving quickly on this sort of thing. Changing domicile sits somewhere between replacing an auditor and updating a pension scheme on the list of matters boards would rather not spend time discussing. That makes the early movers more interesting than their number alone would suggest.

Whether investors care is another question. Domicile rarely features in analyst reports and few shareholders buy or sell a stock based on where it is incorporated. It tends to matter only when things go wrong.

Yet that blind spot has arguably come at a cost. Hong Kong built one of the world's largest stock markets around companies incorporated elsewhere. The result was that many corporate disputes, restructurings and shareholder actions involving Hong Kong-listed issuers were fought in Cayman and Bermuda, leaving Hong Kong with relatively little company law jurisprudence of its own.

Academic work in Hong Kong has long observed that minority shareholder protection comes more from securities regulation and listing rules than from investors actually suing under company law.

Singapore made a different choice. Most SGX issuers are incorporated locally, meaning disputes over privatisations, schemes of arrangement and minority shareholder rights are typically resolved by Singapore courts. Over time, this has produced a substantial body of case law on directors’ duties, oppression remedies and take-private transactions. Many listed Hong Kong companies in contrast often watched those issues be decided offshore altogether.

Re-incorporating a dozen companies in Hong Kong will not suddenly transform minority shareholder rights. Yet it may mean that the next restructuring, privatisation dispute or fight over constitutional documents involving a Hong Kong-listed company is argued before a Hong Kong judge rather than one sitting in George Town. For a market that has spent decades exporting much of its company law, that would be no small change.

Related: China wants its IPO money back

Copyright of Ninepin Limited, 2026