The billion-dollar question hanging over Weibo

Pressure builds on its controlling shareholder

Annual reports are not known for their ability to enthral. Yet somewhere between the accounting policies and the risk factors, companies occasionally disclose something that deserves more attention than it receives.

Weibo may have done exactly that in its 2026 annual filing.

The Chinese social media giant warned investors that there could be a change of its controlling shareholder. On its own, this could read as standard risk boilerplate. But read alongside a series of other filings, it raises a more fundamental question about the financial position of the company that sits above Weibo.

Sina, Weibo’s controlling shareholder, has pledged half of its super-voting shares in the company as security for a syndicated loan. The borrowing itself is a modest US$150m. But it sits alongside hundreds of millions of dollars of revolving loans that Sina draws from Weibo itself.

The disclosures also come against the backdrop of a potentially enormous legal liability. In December 2025 Weibo announced that Cayman’s Grand Court had ruled that minority shareholders in Sina’s 2020 US$2.6 billion take-private had been underpaid. The court valued the company at more than twice the merger price. Sina appealed in late April 2026, but if the judgment is upheld, the liability could exceed US$1 billion once interest is included.

The Weibo board considered the legal development serious enough that it disclosed in the same announcement that a special committee of independent directors had been set up to monitor the implications—not only for related-party transactions with Sina but also for the company’s shareholding structure.

Taken together, this series of disclosures raise a question that appears to have received little attention: how exposed is one of China's largest social media platforms to the financial and legal fortunes of the company that controls it?

Borrowing against control

Weibo’s 20-F filing published in April 2026, which reported the US$150m loan, warned that Sina might pledge more.

If Sina defaults, those shares lose their weighted voting rights (the shares carry 3 votes each), Sina would be left with 31% voting power and would cease to control Weibo, and this in turn could trigger obligations under Weibo’s convertible notes.

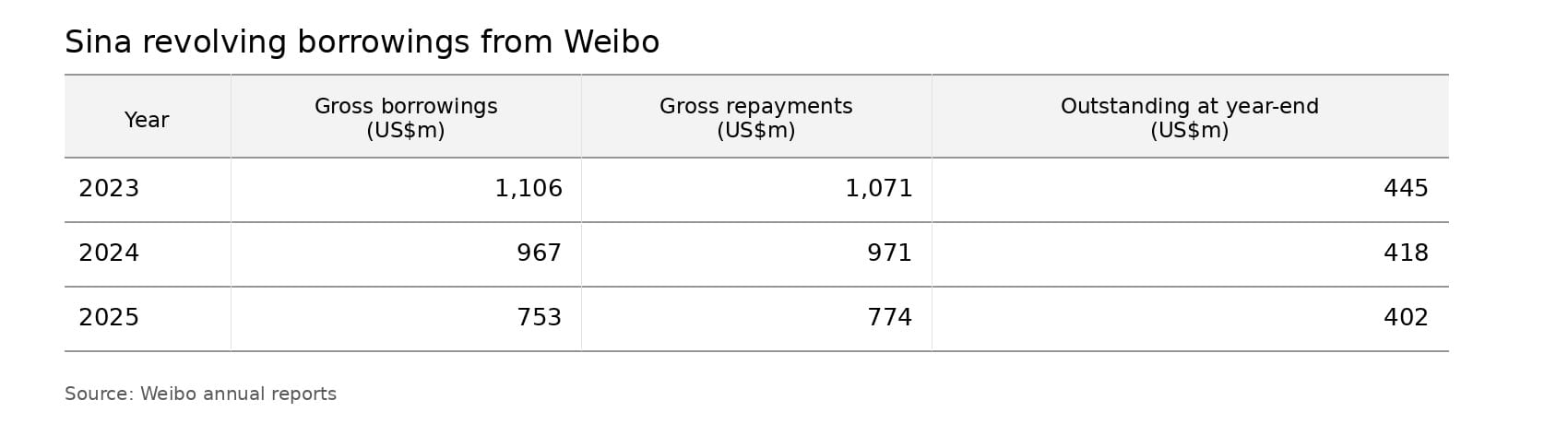

It might have looked like a standard financing arrangement. But in the section on related party transactions, it emerges that Sina is also borrowing hundreds of millions of dollars from Weibo every year:

Despite nearly US$3 billion of annual loan flows over three years, the outstanding balance barely changes at around US$400m. This means Sina is repeatedly relying on Weibo as a source of liquidity and the economic exposure barely changes.

If Sina already has access to hundreds of millions of dollars from Weibo, why did it need to pledge half of its voting control to raise another US$150m from external lenders?

Some answers may lie in the judgment from the Cayman Islands appraisal litigation. Bonnie Zhang, who served as CFO of both Sina and Weibo, gave unusually candid evidence about the group’s finances.

She testified that Sina had “quite limited cash” outside Weibo, initially because of funding demands for its fintech business, and later because “Sina has limited ability to raising (sic) funds for itself.’’ She also said that Sina’s operating cash flow is “not as robust as Weibo” so its ability to repay intercompany loans is limited.

The court drew a striking conclusion: there was “no realistic expectation of repayment” of the loans in the ordinary course of business, observing that Sina was effectively using Weibo as working capital to fund its day-to-day operations.

That finding also places the share pledge in a different light. It no longer looks like a standalone financing arrangement, but part of a broader dependence on Weibo’s cash flows.

The litigation looms large

The market reaction to all of this has been notably subdued. The Cayman judgment was made public on 31 December 2025, the same day Weibo disclosed the decision, announced the formation of a special committee and unveiled a US$200 million share repurchase programme.

Yet the share price edged higher in the following days. While the buyback may have influenced sentiment, there was little sign that investors materially repriced the litigation or the broader financing issues surrounding Sina.

The broader share price shows little evidence that investors have focussed on these issues. Weibo’s valuation has been driven largely by sentiment towards China’s internet sector and the company’s earnings outlook, with the shares declining over the past year despite regular dividends and buybacks.

Analysts continue to debate advertising growth, AI monetisation and user growth concerns. The financing of Weibo’s parent has generated little discussion among investors or analysts.

Its financial health should now be viewed against a potentially significant legal liability. Weibo has provided no further update on the status of the Cayman Islands appeal, although we know from court diaries that the hearing took place on 27 April 2026.

The appeal may succeed or further appears could prolong the litigation. But the legal case has given investors a reason to look again at a handful of disclosures buried in Weibo’s annual report.

Read together, they point to a controlling shareholder under considerably more financial pressure than first appears.

Copyright of Ninepin Limited 2026