Unshackling investors in Japan (2)

What are the pros and cons of the new large shareholder reporting regime? How might different types of investors respond?

Part 2: Looking forward

Several things stay the same under the new regime: investors with stakes of more than 5% must still file a report within five days; increases or decreases of 1% or more must be reported within five days; and financial intermediaries continue to enjoy the more flexible special reporting rules. Core concepts relating to “material proposals” and “joint holders” also remain.

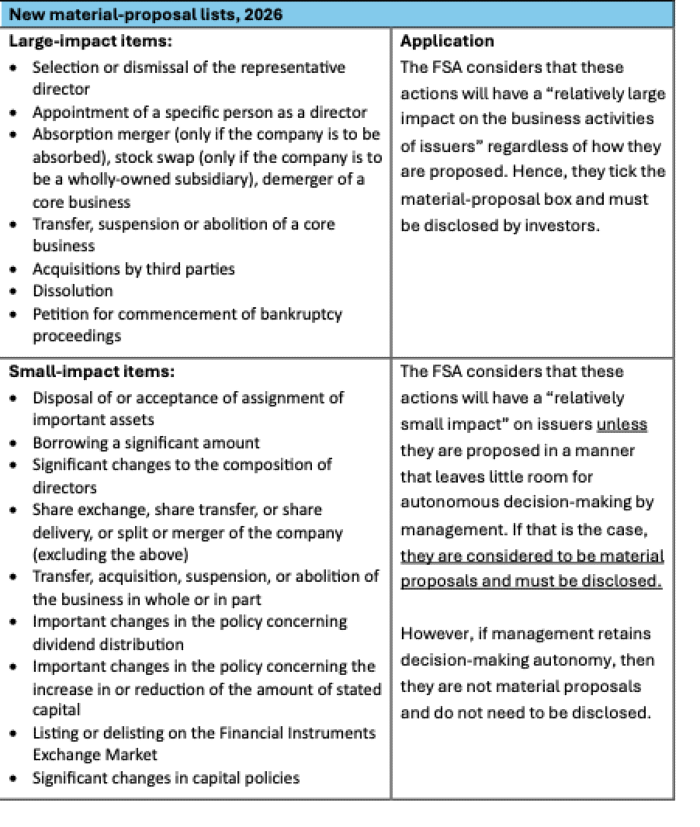

What is changing is potentially far reaching. From May 2026, investors will enjoy considerably more scope to engage companies and exercise their rights without triggering a reporting obligation. To simplify, the list of material proposals is now divided into matters likely to have a "relatively large impact on the business activities of the issuer" (and must be disclosed) and those described as having only a "relatively small impact" (and need not be disclosed).

Control over management

The criteria for inclusion in the large-impact list is anything that has a “high potential to directly affect control over management”, said Tatsuya Taniguchi, Attorney-at-law, TMI Associates, Tokyo and a member of the team drafting the FIEA amendments while on secondment to the FSA. This would include such things as proposals to a shareholder meeting to appoint or dismiss a representative director or a specific director. The rationale is that such proposals, if passed, would leave management with little autonomous decision-making power. They would have to implement them. Hence, these types of proposals would be considered material and have to be disclosed.

In contrast, the small-impact list covers areas where management retains a high degree of discretion, such as setting dividend and other capital policies, or shaping board composition.

It is important to emphasise that the regulator has tried to remove subjectivity in devising these two lists. As TMI’s Taniguchi also told Firefly, “The distinction between “large impact” and “small impact” is based not on the degree of impact on management per se, but rather on the degree of impact on control over management.” To give an example: it is possible that shareholder proposals for changes in capital policies could have a big effect on a company and its management over time, but such recommendations would not change corporate control because management retains the ultimate decision-making authority. They are therefore classified as “small impact”.

This is markedly more permissive than the old regime and a welcome change. As noted in Part 1, it seems unnecessary for the FIEA to constrain what large shareholders can say to companies when management has the discretion to accept or reject these suggestions.

Collective exemptions

Another key change applies to the joint-holder rules, which now include a pragmatic new element called the "Collaborative Engagement Exemption". This is intended to narrow the application of the rules by differentiating in a more nuanced way what constitutes joint conduct, thereby giving shareholders more latitude to undertake collective engagement.

One area is where investors agree to do something such as jointly exercising voting rights, but certain members of the group unilaterally and independently make their own material proposals to a company. This would not be considered joint conduct under the new rules. This is helpful because investment institutions may agree to work together on a specific company issue, but will typically continue their own individual engagement efforts with that company at the same time. Moreover, most participants in collaborative efforts come from the stewardship or ESG teams of investment institutions. They may or may not be able to speak for their portfolio manager colleagues, who will likely be having separate meetings with the same companies.

A second scenario where the exemption will apply is where investors agree to jointly vote against specific resolutions at shareholder meetings, but do not propose anything. Voting against does not equate to proposing and the FIEA now more firmly emphasises the need to make tangible proposals before the joint-holder rules to come into effect. This interpretation is a sensible recognition that investors today often communicate about what to vote for or against at shareholder meetings. If every such conversation and action were subject to regulation, the FIEA would continue to cast a long shadow over stewardship in Japan. It also seems unlikely that such a provision could be enforced in any case.

The third scenario provided is where investors agree to vote together on specific resolutions at a single company meeting in a certain year and, crucially, vote their own shares (ie, do not delegate voting rights to another investment manager). This is called the "individual exercise of rights". However, any general voting agreements spanning more than one year, or multiple companies in one year, would not meet the "individual" test and not be eligible for the exemption. The regulator here is simply trying to distinguish between one-off collective actions and those which are part of a longer term project. Voting your own shares is important because delegation could lead to a situation where one asset manager is voting on behalf of multiple investors, giving them outsized influence in the eyes of the regulator.

All problems solved?

The amendments are a serious attempt to address many of the challenges that mainstream investors face in engaging with listed companies in Japan, especially collectively. Having received official blessing in the 2014 Stewardship Code to become proactive stewards on issues of company governance, investors now have a firmer legal foundation on which to act. The FSA clearly wants to encourage more substantive dialogue between investors and companies. Has it solved all problems with these changes? Not entirely.

One set of concerns, which will not come as a surprise to legal mavens, relates to a lack of clarity in the new rules. Exhibit A is the new list of material proposals itself—see table below. Although separating issues into large- and small-impact categories provides a greater degree of certainty than the old list, which clumped together 13 topics into one broad group, uncertainty is created by overlap between the lists. For example, mergers and transfers of businesses appear in both lists. And there are no precise definitions as to what each item covers. Is the transfer of a core business different from the disposal of an important asset?

It is worth noting too that the small-impact list contains things that could be deemed as material proposals depending on how investors propose them to companies. That is to say, are they verbal or written recommendations to a company that let management decide what to do, or are they formal proposals made to a shareholder meeting that seek to force a certain course of action? In-house counsel will still have work to do.

It will also be interesting to see if the management-autonomy framework turns out to be as clear cut as the new rules imply. One can imagine numerous scenarios in which a group of investors effectively force change upon a company through consistent and effective lobbying on financial performance. Although technically retaining the discretion to act, management may feel compelled to give in to boost their market standing.

Since March 2023 the Tokyo Stock Exchange (TSE) has pressed listed companies to boost their market value through greater awareness of cost of capital and profitability. Those with a PBR of less than 1 have been under particular scrutiny and the TSE has been urging investors to engage actively with them. Now that many companies have achieved PBRs of 1, the focus is on lifting the ratio higher. Capital management is absolutely in the wheelhouse of management under the FIEA amendments, yet it is also the subject of quite intense regulatory and market scrutiny.

Japan meanwhile has witnessed many cases where shareholder pressure has forced recalcitrant companies to make fundamental governance reforms. One of the more famous cases took place in 2013 when shareholders of Canon opposed the re-election of its dominant chairman, Fujio Mitarai, by an unheard of 28% vote against—a reaction to the company's refusal to appoint independent directors. Shortly afterwards it did. A decade later Mitarai had a narrow escape when 49.41% of votes were cast against him in 2023 over anger at Canon's lack of a succession plan and slow pace of board refreshment. The company later committed to appointing new independent directors and being more transparent about succession.

The point here is not to undermine the new management-autonomy concept, which we believe introduces a sensible degree of pragmatism to the large shareholder system in Japan. It is simply to note that it may not always be as binary as officials expect and could become a reason, or excuse, for investors not to take action.

To be fair, the FSA appears to have anticipated some of these objections in its Q&A document from August 2025. It outlines various scenarios in which investors commonly seek to engage companies and which would not, in its opinion, constitute an attempt to bring about significant changes in companies in most circumstances. These include:

· A proposal to sell strategic shareholdings, phrased either generally or in regard to a specific stock;

· A proposal to create a succession plan for representative directors or changes to the policy regarding their nomination, selection, and dismissal processes;

· A request to increase the number of independent directors in line with the Corporate Governance Code;

· A request that an issuer reviews its business portfolio and considers restructuring its assets (unless the proposal is specifically intended to have a significant impact on the company).

While these examples are helpful, the words in italics once again underline that a degree of uncertainty will remain in the new rules.

The Institutional Investors Collective Engagement Forum (IICEF) echoes some of these concerns. While agreeing that the overall direction of these reforms is positive, their concern is that defining what constitutes a material proposal is always going to be incomplete. "Companies will always face new issues. We do not know what will happen next. If the FSA updates (the Q&A), it will be OK. But the duty time of each official is short. They should continue to add examples (to the Q&A)," said Yuki Kimura, chairman of IICEF.

The group is also not satisfied that a grey area remains over the issue of business asset restructurings, a topic included in both the large- and small-impact lists. "This is the most important matter in Japanese companies these days. The businesses where investors will most likely worry about negative impacts to corporate value will probably be included in the “large-impact items”. So we still have to be very careful about telling companies to sell businesses," Kimura said.

A solution to this conundrum—and a way to avoid the FSA having to devise an ever-longer list of material-proposal examples in future—would be to allow investors to discuss any topic with companies under the large shareholder system without triggering a reporting obligation. A disclosure obligation would only be required if investors planned to take tangible legal action to force change upon a company, such as putting forward a proposal at an annual shareholder meeting, calling for an EGM, or launching litigation. Since such disclosure is already mandatory and routinely implemented, this would be in line with current practice and pose no additional transaction costs. Importantly, this solution would not eliminate the requirement for newly minted large shareholders to explain their purpose of holding.

Would such a reform work at this stage? Almost certainly not, according to Tatsuya Taniguchi of TMI Associates (whom we quoted earlier in this article). While acknowledging the practical value of such a suggestion, he noted that the obstacles were more political and financial. "From the FSA’s perspective, revisions to the TOB (tender offer bid) rules or the large shareholder reporting rules require an enormous amount of resources and highly specialized expertise. Given the many other competing priorities, it has been difficult for the FSA to allocate sufficient resources to these areas... Accordingly, it is unlikely that another amendment will be undertaken in the immediate future." Other legal observers have noted that a degree of vagueness is ever-present in Japanese regulation and that is how the government likes it.

Nevertheless, investor groups need to take a longer term view and continue to advocate for reform where the system is becoming clogged by unproductive complications.

Investors unleashed?

How will the diverse investor community respond to these landmark reforms? For a range of reasons, both internal to the investment community and as a result of macro external forces, we think the status quo will hold for a while. A useful way to frame this discussion is to segment the community into its main constituent parts.

Starting with activists, it seems unlikely the FIEA amendments will have a major impact on Japanese groups like the Murakami funds, Effissimo Capital, Strategic Capital, and 3D Investment Partners, or on foreign activists such Oasis, Elliott, and Value Act. Their campaigns are highly visible already. By definition they need to generate publicity to communicate their ideas, push put pressure on management, create excitement around a stock, and garner support for resolutions put to AGMs.

Activists know how the system works and use it to their advantage. To avoid implicating other investors in a joint-holder group, they make explicit in campaign material that they are not soliciting votes or joint action of any kind. As Oasis said in its presentation, “A Better Kao”, in December 2024:

“Oasis has created these materials for informational purposes to educate the public and shareholders of Kao… Oasis is not and should not be regarded or deemed in any way whatsoever to be (i) soliciting or requesting other shareholders of Kao to exercise their shareholders’ rights (including, but not limited to, voting rights) jointly or together with Oasis…”

Indeed, it is rare for activists to formally collaborate with each other or mainstream investors on specific company cases, including putting their names on group letters to companies (though they occasionally sign letters on policy issues). The word on the street, however, is that some activists are working with private equity funds to help take companies private.

Foreign passive

At the other end of the spectrum, it seems equally unlikely that the big foreign, passive houses, namely BlackRock, Vanguard, and State Street Global Advisors among others, will alter their stewardship policies or modus operandi in any significant way in the near future in response to the FIEA amendments. Their huge size and internal policies have long militated against explicit involvement in collaborative engagement, in part due to strict concert-party rules in the United States.

They are also careful to frame engagement with companies as primarily an information-gathering tool. As BlackRock Investment Stewardship (BIS) said in a recent “Investment Stewardship Global Engagement Summary Report” for Q1-Q2 2025:

“BIS does not view engagements as a mechanism to effect change, but to inform our voting decisions.”

BIS manages stewardship for the firm’s index equity strategies, which account for 90% of almost US$7 trillion under management in public equity assets. Another unit called BlackRock Active Investment Stewardship manages the active component.

The backlash against “ESG wokery” in the US in recent years, including state lawsuits against asset managers, has boxed in the big passive houses further. In December 2024, BIS released its updated 2025 Global Principles and, among other things, removed references to the value of gender and racial/ethnic diversity on boards. Vanguard and SSGA similarly toned down diversity aspirations in their 2025 voting policies. Having used the word “diversity” 16 times in the board composition section of its 2023 Global Principles, BIS referenced it just once in the 2026 version:

“We note that in many markets, policymakers have set board gender diversity goals which we may discuss with companies, particularly if there is a risk their board composition may be misaligned.”

This was in part a reference to Japan. Accordingly, BlackRock’s latest voting policy for Japan, dated April 2025, briefly references diversity and women directors in relation to the government’s 2023 policy that companies should aim for 30% gender diversity in boards and executive management by 2030. The actual substance of the BIS voting policy is relegated to a footnote.

Local passive

Japanese passive investors are more collaborative. The Institutional Investors Collective Engagement Forum (IICEF), quoted above, was formed in 2017 and brought together six large institutions, including the Pension Fund Association (PFA). The rationale was as much practical as ideological: being passive meant low fees and small budgets for stewardship work, so pooling resources made sense. But due to the restrictions around making material proposals and acting as joint holders, IICEF initially felt compelled to limit itself to writing to companies and asking questions on topical governance and ESG themes.

IICEF freely admits to taking a conservative and careful approach to engagement, yet has gained traction over the years in getting companies to speak. It now meets three to four companies a month, usually with senior executives. Significantly, requests to meet independent directors have largely been rejected—something that foreign investors have managed to achieve (see below).

How will IICEF respond to the FIEA changes? One member said that while the Forum will continue doing what it has been doing in recent years, the environment for company engagement has opened up considerably—not just because of efforts by the FSA but also the Ministry of Economy, Trade and Industry (METI) and the Tokyo Stock Exchange (TSE). Specifically, it is now easier to address previously sensitive areas such as cost of capital, shareholder value, share prices, and return on equity (ROE). Although IICEF and other investors had been raising these issues for many years, it was only when TSE joined in that "everyone looked in the same direction", he added ruefully.

Local active

The story is more fragmented among domestic active managers. Although all major houses have signed up to the Stewardship Code and engage companies individually as required, the extent of collaborative engagement is limited. This is principally due to conflicts of interest created by commercial relationships between their parent companies, typically big banks and insurers, and listed issuers.

The paucity of collaborative engagement is reflected in an annual survey of members of the Japan Investment Advisers Association (JIAA). In late 2024 the association reported that only 26 companies (31% of respondents) had joined collaborative engagements, while a further 15 (18%) indicated they planned to do so. The remaining 42 firms (51%) declared they had no intention to participate either because "they handle matters individually and see no need" or because "barriers, risks, or issues exist in collaborating with other investors, making implementation or continuation difficult". These barriers and risks specifically related to "unclear determinations" as to whether actions constituted material proposals and joint ownership. It is worth noting that the collaborative engagement that does take place focusses mostly on climate change and the environment, not the more sensitive issues of governance and financial performance (which firms leave to their individual engagement efforts).

The numbers improved slightly in JIAA’s most recent survey published in late 2025, with concerns remaining largely the same. But the association also noted that “awareness has significantly improved following the 2024 amendments to the Financial Instruments and Exchange Act”, suggesting a possible (though likely incremental) uptick in collaborative engagement in future.

One of the challenges facing active managers is the lack of a dedicated organisation able to advocate for better corporate governance in Japan. While there are well-established discussion groups, notably the Japan Stewardship Forum, there is no equivalent of IICEF. Although JIAA could theoretically take up the mantle, as an investment industry association that would be highly unlikely. Its primary role is to promote the investment industry, not be a reforming advocacy group.

Another thought is that the FIEA amendments might spur the formation of a new homegrown advocacy group, although the chances of this seem slim. It would probably take the FSA to light this particular fire, but that is definitely not on the agency's agenda. Resistance from the Keidanren, the conservative business federation, as well as the banking and insurance sectors would likely be fierce. In other words, such a group would immediately run up against restrictions imposed by financial holding companies on asset management subsidiaries to vote or act independently.

Foreign active

So that leaves active mainstream foreign investors. They at least do not suffer from the lack of member organisations coordinating collaborative regulatory and company advocacy. The two main entities in the governance space are the Asian Corporate Governance Association (ACGA), based in Hong Kong, and the International Corporate Governance Network (ICGN) in London. Other entities operate more in the sustainability, ESG or climate arenas, including the Principles for Responsible Investment (PRI), named after its foundation document, and the Asian Investor Group on Climate Change (AIGCC), based in Sydney. (Note: All these groups also have passive managers as members.)

After the cold shower it inadvertently gave foreign shareholders with the 2014 clarification, the FSA tried reassurance. "We think there is huge room for you to do collective engagement", one agency official told ACGA in 2016. In the same year the Association created a Japan Working Group that focussed primarily on regulatory policy and later initiated a programme of engagement with systemically important companies in 2021.

With all this organisational firepower, will the amendments boost enhanced foreign investor dialogue with companies? Probably not as much as one might hope, at least over the short term. While foreign active managers will welcome the less restrictive FIEA rules, regulation is only one driver of action. This group faces a host of headwinds globally, from budgetary constraints on stewardship work to ongoing political pressure to dial down ESG and sustainability/climate expectations, continuing low economic growth in many home markets (often accompanied by a watering down of shareholder rights), uncertainties around inflation, and the sustainability of soaring tech-driven stock prices. This is all in addition to the increasingly dangerous geopolitical games being played by major nations.

Every major global investor Firefly has spoken to over the past year, with the exception of some well-heeled activists and one large US asset manager, is having to cut back their stewardship budget and sweat each engagement dollar harder. Japan may be less affected by these trends, given the strong performance of its stock market, but it is unlikely to escape entirely. Asset managers there are in some ways a victim of the market’s success: the value of their funds may have risen, but with so much uncertainty around they are not necessarily being given more resources to do their jobs.

There remains plenty for investors of all stripes to be doing in Japan. Governance reform remains a work in progress—the CG Code arrived only 10 years ago and is about to undergo what appears to be a significant revision, not necessarily for the better. Boards are still in transition, director training is limited, and corporate leadership needs more rejuvenation. Asset restructurings, reduction of cross-shareholdings, a greater focus on capital efficiency and corporate value, fairer M&A—there is no shortage of big issues for investors to focus on. Whether they choose to take up the challenge or not, the FIEA amendments give them a bigger seat at the table.

End of Part 2.

Copyright: Ninepin Ltd, 2026