Toyota tests the system, falls short

Despite a higher offer price for Toyota Industries Corporation (TICO), surprising weaknesses in Toyota Motor’s handling of the TICO privatisation remain. While this case says much about the Toyota Group’s governance culture, it also points to a range of flaws in the squeeze-out process in Japan.

Squeeze-outs in Japan: Part 1 of 3

Much has changed in Japanese corporate governance (CG) over the last 15 years. It wasn’t that long ago when the independent-director concept was dismissed as culturally unworkable and of no use, not least by powerful companies such as Toyota and Canon and business groups like the Keidanren. It is now accepted as a core input for better governance, as are other ideas like capital efficiency and sustainability disclosure. Cynics may view the pivot on independent directors as a classic attempt to please international capital markets—and there is some truth in that. But it also an experiment in building a higher performing corporate sector, facilitated by a generational shift to younger policy makers, investors and business leaders.

Something had to give in Japan in the first decade of the 2000s. Its ageing and often ultra-conservative business leaders, still traumatized by the collapse of asset prices in the late 1980s and subsequent deflation, were playing things too safe. Companies were fanatically hoarding cash, boards of directors were extraordinarily large (sometimes 40- to 60-people strong), and many issuers were more concerned about keeping executives employed and comfortable in retirement than creating value for society. Unlike other developed markets, Japan jumped into CG reform not to rein in animal spirits but to unleash them.

One other key point of difference: Japan has been trying to address its actual CG challenges, not merely using reform to paper over existing ownership structures and poor governance. One of its biggest tasks now is promoting corporate restructurings to encourage companies to shed underperforming businesses and create new opportunities through acquisitions and privatisations. Closely linked to this is the issue of cross-shareholdings—interlocking equity holdings within and between large business groups. At worst these tie up capital, constrain management autonomy, create governance conflicts of interest, and weigh on valuations.

To stimulate as much domestic M&A as possible, the Japanese government has sought to create a stronger enabling framework. It has amended company law on several occasions to make transactions easier, which is good for business. It has twice introduced new guidelines on what constitutes fairness in such deals, which is good for investors.

But there isn’t any room for complacency: compared to other developed markets, the privatisation process in Japan is harsh on minority shareholders; and despite being widely adopted by companies, the fairness framework has some big holes and is due an update. CG reform is still a work in progress.

This is the context in which the privatisation of TICO sits. Like other similar deals, it is a two-step process: a tender offer, which started in mid-January 2026, followed by a “squeeze-out”. Although Japan bases its squeeze-out system on the US, minority shareholders lack the high-level of judicial oversight provided by the Delaware courts and their much tougher fairness process. Nor do shareholders in Japan enjoy the strict thresholds for squeeze outs found in Anglo/European markets, such as court-approved schemes of arrangement and the 90% equity ownership trigger. Controlling shareholders in Japan can squeeze out minorities once they reach a relatively low 66.67% stake. The EGM vote to approve this is a mere formality.

The unique aspect of the TICO privatisation is that it is taking place within the Toyota Group. The country’s leading company has always been something of a law unto itself when it comes to governance and this deal reflects that reality. It is not being led by Toyota Motor, but a small unlisted real-estate affiliate called Toyota Fudosan. Opacity cloaks many aspects of the transaction from why Fudosan is nominally in charge to the expected business and financial synergies. Remarkably, the Toyota Motor board has had little public to say. It is not surprising that foreign shareholders of TICO have been upset and vocal about the offer price. Nor is it surprising that their domestic counterparts have been quieter. “It’s Toyota!”, one shrugged.

To add more nuance, it is worth noting that while many domestic investors think the structure of this deal is far from ideal, they view it as a “necessary evil” to address cross-shareholdings within the Toyota Group and “ensure the sustainable growth of Japan’s biggest company”, as one Tokyo market insider said. This is especially true for passive investors whose long-term performance is more dependent on large caps such as Toyota.

Given the complexities of these issues, we are dividing our analysis into three parts. This first article looks at key governance questions raised by the TICO deal. A second will assess how the system of squeeze-outs in Japan compares to other major markets: despite improvements, it is tougher on minorities. The third will examine the M&A fairness framework and what could be done to make it more robust.

A game of two halves

Toyota Fudosan’s first tender offer price for TICO in early June 2025 of ¥16,300 per share—prior to finalizing complex overseas regulatory requirements—was roundly criticised as being too low. Not only was it below the market price at the time of ¥18,400, shareholders said it compared poorly against the average 44% premium paid in similar take-private deals in Japan: the TICO offer was just 23% above the company’s price before news leaked about the tender offer in late April 2025.

Fudosan and TICO countered that the market price had been manipulated following the leaks and defended the offer as fair. Much of their argument was based on “fairness” procedures that TICO put in place to scrutinise the transaction: a special committee of its board made up of independent directors; the use by Fudosan, TICO and the Special Committee of independent legal and financial advisers; no attempt at coercion of shareholders; the use of a “majority of minority” condition; and an ultimate squeeze-out price equal to the tender offer price, so that shareholders who did not tender their shares would not be disadvantaged later. This framework essentially followed a set of “Fair M&A Guidelines” published by the Ministry of Economy, Trade and Industry (METI) in June 2019 and used by numerous other companies since.

Yet shareholders of TICO and Toyota Motor Corporation (TMC) were upset not just by issues of price. They were harshly critical as well of the governance of the process, especially the role of the Special Committee. Criticisms ranged from the committee not trying hard enough to get a better price from Fudosan to questions about its competence, the lack of a “sum of the parts” (SOTP) calculation in valuing TICO (important because like most Japanese companies it holds assets valued at historic not current prices), and the absence of a fairness opinion. Foreign shareholders felt shortchanged and complained vigorously to Toyota Motor and TICO (see the letter from the Asian Corporate Governance Association to both companies in August 2025).

This was the state of play until Elliott Management, an activist US fund with a penchant for litigation and close ties to the White House, ran onto the field. On 11 November 2025 Elliott confirmed it owned a “significant” stake in TICO following the latter’s disclosure to the market that the activist held a 3.26% stake as of end-September 2025. In its statement, Elliott said it believed the “proposed transaction very significantly undervalues Toyota Industries and reflects a process that has lacked transparency and has fallen short of proper governance practices”. On 11 December it announced an increase in its stake to 5.01%, making it a large shareholder for reporting purposes.

A few weeks later, in mid-January 2026, Toyota launched its formal tender offer with an improved price of ¥18,800 per share, close to the then market price and 15% above its initial “final” offer in June 2025. Not surprisingly, Elliott and some other shareholders have rejected the higher price, saying it still substantially undervalues TICO. The US activist upped the ante again by increasing its stake to 6.65% in January 2026 and later that month published a presentation arguing that TICO’s intrinsic net asset value was more than ¥26,000 per share. Elliott also put forward a “Standalone Plan for Toyota Industries”, which it claims “offers a far more compelling option for shareholders than the Revised TOB (takeover bid)”.

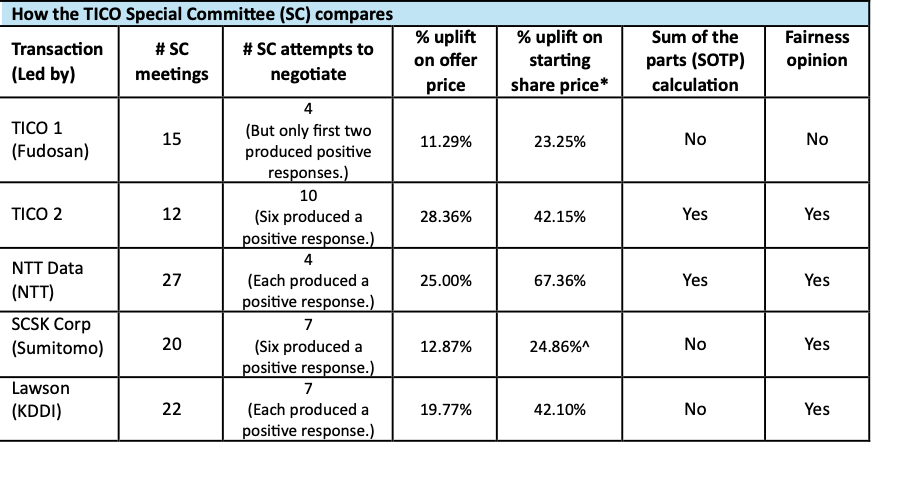

However this contest turns out, one of its most fascinating and concerning aspects is Toyota Motor’s governance of the privatisation. Despite the pricing upside for shareholders and apparently sincere efforts by the TICO board and its Special Committee to get a better deal, TMC and Fudosan have displayed a notable stubbornness in sticking with former positions. They have not, for example, taken the opportunity to be more transparent as to why Fudosan is leading the transaction, nor elaborated further on the expected synergies. The Fudosan board also dragged the Special Committee through 10 more rounds of negotiation before agreeing to a final offer in line with the market price (in fact, a 4.42% premium at the time). Surely they could have reached this point sooner.

Other factors are troubling too. The TICO board and its Special Committee listened to investor criticism and asked their financial advisers—SMBC Nikko Securities and Mitsubishi UFJ Morgan Stanley Securities, respectively—to undertake an additional DCF-SOTP valuation (with discount rates and terminal values disclosed) and provide a fairness opinion. TICO also engaged a second adviser, EY Strategy and Consulting, to do a valuation and fairness opinion. In contrast, Fudosan chose not to request its financial adviser, Nomura Securities, to do the same. Its second-round valuation ranges are therefore significantly lower than those from TICO and its Special Committee, nicely providing dissident shareholders with the ammunition to keep fighting. And it has doubled down on its unconvincing interpretation of the “majority of minority” standard. We explore these issues further below.

Why Fudosan?

The formal rationale for putting Fudosan into the driving seat is that it is independent of the auto industry and in a better position to oversee the integration of TICO into the wider group. Toyota says its strategy is to evolve into a “mobility company” that encompasses not just auto and vehicle production, but the full gamut of physical transportation of people, goods and energy, and digital delivery of related information services. Giving this role to Toyota Motor or one of its main auto affiliates, namely Aisin or Denso, would be inherently limiting, the company argues.

Why is this? Because if TMC, Aisin or Denso took the lead “they are likely to get caught up in the perspective of automotive OEMs”. With 68% of TICO’s business coming from a non-auto business—making forklift trucks and selling related services—Toyota argues that it needs to use a different offeror if it is to actively incorporate “innovative ideas and diverse perspectives, beyond the boundaries of industries”. As a more independent company, Fudosan can serve as an “intermediary to facilitate smooth collaboration in business operations among Toyota Group companies”.

None of these arguments is particularly compelling. Toyota only briefly explains what it means by a “mobility company”—this section in the initial tender offer notice from June 2025 is just a few pages long and is replicated in the final notice from January 2026. It is not clear that Fudosan has the management expertise and depth to manage such a gargantuan task. Nor has Toyota provided much narrative on how Fudosan and TICO will manage the transition to a mobility company, or given any analysis of the potential financial gains to be made from the expected synergies.

So why Fudosan? One factor at play is to reduce scrutiny on Toyota Motor and its board. Were TMC in the driving seat, its directors would have to be more publicly involved and forced to answer questions. For example, why isn’t TMC taking a voting equity stake in the future holding company that will own TICO outright? Without this, the upside for TMC shareholders is limited and their only tangible reward will be a guaranteed dividend from non-voting preferred shares that Toyota Motor will buy.

Such scrutiny would have been driven as much by market convention as regulation. Strictly speaking, TMC is not a controlling shareholder of TICO—its stake is not a majority of the voting rights but just under 25%—so this transaction is not subject to either the “Fair M&A Guidelines” (2019) from the Ministry of Economy, Trade and Industry (METI) or more recent revisions to the listing rules of the Tokyo Stock Exchange (TSE) on “MBOs and Subsidiary Conversions” in April 2025.

Yet the market still expects Japan’s #1 company to play by the highest standards and set an example. Indeed, the Guidelines state that the actual application of the “controlling shareholder” definition should be “determined substantively on a case-by-case basis, taking into account the spirit of these Guidelines”.

A second reason is that Fudosan is much more than a real-estate company, according to market observers. It is fast becoming a pivotal player in the Toyota Group ecosystem.

Signs of something bigger at play came when high-flyer Kenta Kon, TMC chief financial officer and board director, was concurrently appointed to the board of Fudosan in June 2021. “His appointment to Fudosan caught everyone by surprise. But when you see this deal (TICO), you begin to understand”, one investor said. As Mr Kon told the inhouse Toyota Times Business website in June 2025 when asked about the rationale for the deal structure: “Toyota Fudosan’s shareholders are comprised of 15 Toyota Group companies. More than Toyota Fudosan, this can be viewed as an investment by the Toyota Group.”

If Fudosan is to become a strategically important holding company within the Toyota Group, the TICO deal would have been an opportune time to explain this to the market.

Special Committee redeems itself

Special committees are a fairness measure promoted by the METI 2019 guidelines and are now widely adopted in Japan. Such committees can comprise either independent directors of the company, outside experts, or both. Their job is to ensure the fairest possible deal for the company and its shareholders. In TICO’s case, the three members were all independent directors on its board.

Many of the initial criticisms of the Special Committee were fair. It should have pushed its financial adviser, Mitsubishi UFJ Morgan Stanley Securities, for an SOTP valuation and a fairness opinion. It should have required the firm to undertake its own due diligence on TICO, rather than rely solely on information and numbers provided by management. And the committee could definitely have tried harder in the price negotiations: it only sought to negotiate four times with Fudosan over late April to late May 2025, achieving a modest 11.29% uplift on the initial offer price of ¥14,646. The first two negotiations produced a higher offer price, the latter two were firmly rebuffed. The committee then pronounced the result as fair to shareholders.

Other aspects are less black and white. Even if committee members were more expert in privatisation deals, it is likely they would still have underperformed the first time around. Independent directors in Japan do not generally have the influence in companies that their counterparts enjoy elsewhere. Nor do special committees in Japan have the practical power to say no to transactions (a key principle under Delaware law), whatever the M&A guidelines say.

Moreover, the TICO committee was negotiating with the Fudosan board, which happens to be chaired by Akio Toyoda, chairman of TMC and scion of the founding family. This board has only four members, all men. No independent directors. No committees. And Mr Toyoda is investing his personal money in a 0.56% stake in the holding company buying out TICO. He therefore directly benefits from a lower price—a huge conflict of interest that TMC has never sought to address.

Still, shareholders were right to be disgruntled and their criticisms clearly hit home. The following table compares the TICO committee’s first and second round performances against three other major deals from 2024 and 2025.

Despite the Special Committee’s improved performance, some obvious questions remain. Why didn’t it fight for a better deal from the start? The committee faced tough opponents, true, yet appeared to underestimate TICO shareholders. An offer price 11% below the market price should have been more of a red flag.

Why wasn’t Toyota Motor itself more sensitive to issues of price as well as investor expectations for more sophisticated valuation methodologies and a fairness opinion? TMC could say that fairness opinions only became mandatory under the TSE listing rules in mid-April 2025, shortly before it went public with its initial tender offer announcement. Yet the Lawson deal provided such an opinion more than a year earlier. A degree of insensitivity was also apparent in the contrast between the efforts of TICO and its Special Committee to seek SOTP valuations and fairness opinions in preparation for the revised tender offer, while Fudosan did not.

An unnecessary complication

Without question the most idiosyncratic part of this whole deal from a governance perspective has been Toyota Fudosan’s interpretation of the “majority of minority” concept, first introduced to Japan in 2019 by the METI guidelines.

To put it simply, when undertaking a change of control, the offeror should ensure that a majority of “general shareholders” (those not affiliated to the controlling shareholder or management) support the deal. This can be done in one of two ways: by getting more than half of these shareholders to tender their shares during the offer period or by allowing them to approve the transaction through a vote in an extraordinary general meeting.

On the basis that they are “independent third parties who have no (financial) interest in the Offeror” (ie, the holding company to be formed), Fudosan decided to include the three group companies—Aisin, Denso, and Toyota Tsusho, a trading firm—in the “general shareholder” category. After being heavily criticised for this decision, Toyota officials publicly repeated that the three companies were independent entities and had freely decided to join the deal. This stretches credibility and conflicts with at least two broad realities: TMC owns 20-22% of each of the three companies (they are therefore close affiliates, though not subsidiaries) and each is an integral part of the TICO privatisation process and the future mobility company envisaged. A veteran legal observer called this interpretation “outrageous”.

In the final tender offer notice, Fudosan doubled down. It repeated the independent-entity argument and said, "The communications of their respective intentions to tender their shares in the Tender Offer were made as a result of sincere discussions and negotiations conducted at arm’s length…” It added that the three companies were “not restricted from changing their intentions” regarding participating in the offer.

Since Fudosan’s strategy doesn’t pass a basic investor smell test, what is Toyota thinking? An investor in Tokyo who follows the automaker closely gave an interesting explanation: in claiming the three group companies are independent entities, Toyota gives them agency. “By promoting this as an independent process, it helps to convince the companies to get on board. Nobody outside Toyota thinks this is an independent process. But if it were a group-directed thing, it would get questioned (internally). The key question is synergy, which TMC would have to answer.”

Be that as it may, Fudosan did not need to invoke this vague norm. The “majority of minority” concept is not a rule in Japan, but merely a best-practice suggestion from METI. This is amply reflected in the fact that not all companies apply it in mergers and acquisitions, and some of those who do subsequently ignore their failure to achieve it—for which there is no regulatory penalty. That Toyota believes it can define “general shareholders” however it wishes highlights how unformed this concept remains.

Moreover, the hard arithmetic of squeeze outs in Japan shows that Fudosan could have achieved a majority of genuinely independent shareholders with only a slightly higher tender offer target. Needing 66.67% to secure a two-third ownership majority to pass a squeeze-out resolution in an EGM, then subtracting TMC’s 24.66% stake in TICO, the real-estate company set a minimum percentage of shares to be purchased at 42.01%. It claimed that achieving this figure would be enough to pass the “majority of minority” test.

But what if Fudosan had sought to achieve a genuine majority of general shareholders and excluded Aisin, Denso and Toyota Tsusho from the calculation? Here are the steps:

1. Adding the combined stakes of TMC (24.66%) plus Aisin, Denso and Toyota Tsusho (12.21%), Fudosan’s own stake (5.42%) and Akio Toyoda’s small parcel (0.05%) produces an aggregate Toyota Group ownership in TICO of 42.34%. Hence, general shareholders hold the remaining 57.66%.

2. To achieve a majority of minority, Fudosan would need just over half the 57.66%—in other words, 28.84%.

3. Add 28.84% to the Toyota Group’s 42.34% stake results in a total of 71.18%.

4. To properly compare with Fudosan’s “minimum percentage of shares to be purchased”, subtract TMC’s stake of 24.66% from the total and you are left with 46.52%.

In other words, had Fudosan aimed for 46.52%—a mere 4.51% above its original target—it would have achieved a real majority of the minority. Our bet is that it can achieve this, since it already has the other Toyota Group stakes in the bag and a lot of friendly domestic (and probably foreign) shareholders too—especially now with the higher offer price. Why double down on a bad idea and incur the wrath of your shareholders when you do not need to?

Copyright: Ninepin Ltd, 2026

Coming next: Part 2 on the harsh realities of squeeze-outs in Japan for minority shareholders; and Part 3 on how the "majority of minority" concept and M&A fairness rules could be made more robust.