Macro governance, not AI, is the real story

AI-linked equities have set the tone for Asian markets in 2026. But the more important story is about governments.

AI-linked equities have set the tone for Asian markets in 2026. With help from global investors, they are channeling a positive vision of an AI- and tech-led future that has only sporadically been punctured by bad news in markets with LNG risk exposure.

As alluring as these themes are, the more important story is the way that Asia’s financial market fundamentals are being rewired to put governments back in the driver’s seat. We’re witnessing a pivot toward state-directed capital investment and market intervention that will change the governance playbook across the region.

Over the past two decades, the privatisation of state assets and market liberalisation shaped Asian markets and spurred the rise of corporate governance. But now, we are headlong into a period when macro governance—shaped by government, bank, and private capital flows—is changing the investment dynamic of Asian markets.

The building blocks for this period don’t depend on a global rule book. Instead, long-term performance will rest on investors’ ability to navigate concentration risk in the key indexes and the returns on state-directed capital. It will also raise important questions about how we assess the political capital wielded by leading companies, private equity, and national investors.

A tech-heavy diet with an energy tax

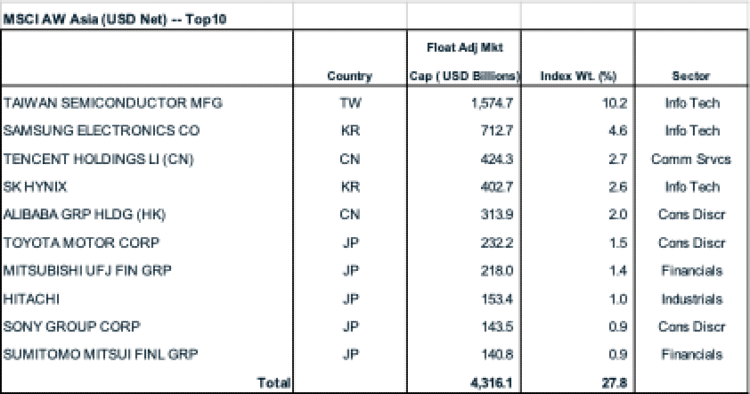

The case for looking at macro governance starts with markets. Whether it’s TSMC, Samsung, or Hitachi, the AI winners dominate the indices along with the top tier industrial companies that provide the infrastructure. They can all make an outsized call on support from their home governments—and the countries where they invest—for preferential regulatory and financial support.

Some like Toyota loom large in the minds of regulators and can set the tone on how the market is perceived for good or ill. Others like TSMC dominate their country’s diplomatic agenda. But this list of companies only hints at the broader macro governance issues that will challenge us in 2026 as corporate and policy leaders pivot to support national policy agendas, defend market access, and protect their legacy global assets.

Asia's large-cap momentum leaders

Source: MSCI, Feb 2026, https://www.msci.com/indexes/index/301700

When markets are offering binary outcomes, with North Asia on strong footing and Southeast Asia treading water, it’s only natural that policymakers are driven by existential policy fears. Market regulators cannot control geopolitical uncertainty, so they are rightly focused on doing everything possible to ensure that their market is investible—and relevant.

The rise of crypto, gambling apps, and now prediction markets means that Asian retail investors are leaving regulated trading platforms and diving into unregulated playgrounds. This has shifted the regulatory agenda, and no market operator wants to be on the wrong side of a politically charged discussion about a shrinking IPO pipeline or misdirected enforcement that gives foreign investors a reason to stay away.

The impact of high stakes policy choices is evident in many markets. Hong Kong and Singapore remain locked in combat to prove their strategic relevance as global financial centres. But they each hold different cards. HKEX and the SFC are under no illusion that their main job is anything but supporting the come-home/stay-home IPO surge and to mobilise fresh capital for homegrown innovators that can give leading China-focused PE funds credible exits. If that means lower listing standards to grab new era AI listings, so be it.

No one should expect Singapore to mimic Hong Kong. Its IPO pipeline is far too small and lacks China as a strategic anchor. Singapore and other market operators will doubtless lower listing standards to look like their peers, but Singapore’s opportunity rests on the city state’s status as a regional investor and bank-led financial hub.

For investors interested in a case of something to avoid, Indonesia is the standout example. First came months of speculative gains after insider-heavy stock volatility hijacked the index in 2025. This set the stage for a major sell-off in January 2026 when MSCI formally putting the regulators on notice that new rules covering better disclosure on the free float of listed issuers are a minimum requirement for future index inclusion. After a round of finger-pointing, heads rolled, and the President has promised that OJK will turn a new page. This is not a fight that Indonesia’s top leadership can afford to lose.

Can we please talk about political capital?

Incidents like the MSCI fiasco in Indonesia are an apt reminder that the geopolitical stakes have rarely been higher for Asian governments. It also highlights the importance of finding a new lens for analysing the choices that governments and companies will be making in this turbulent period.

Analysts are trained to pick winners and losers based on financials, sector and market dynamics. Strategy also factors into the calculus and lodged squarely at the centre of any bet on execution is political capital. How companies accumulate and manage their core political resources can directly influence their ability align with and benefit from government priorities.

This is more relevant than ever given the pressure on Asian governments to channel fresh capital to new AI- and energy-linked national priorities. Whether it’s data centres or new power grids, Asia’s messy track record of “public-private” collaboration will now be put to the test. This will call on investors’ ability to make credible judgements about the stability of policy drivers and the financial impact of state-directed capital programs on company balance sheets and share price performance.

For example, Japan is under aggressive pressure from the Trump Administration to funnel money into new US-based manufacturing facilities. As a result, JBIC and the leading Japanese banks are standing ready to fund SoftBank, Hitachi, and Mitsubishi to name just a few on the list of companies that may participate in the $550 billion investment program.

It’s anyone’s guess how this program will be managed or if the progress will be subject to ongoing disclosure. Controversy broke into public view during Prime Minister Takaichi’s mid-March 2026 visit to the United States concerning the terms of Softbank’s $33 billion deal to build a gas-fired power plant in Ohio. SoftBank’s Masayoshi Son has put his political capital with the Trump Administration on display. Now the question is whether he has similar clout at home.

A very different version of the political capital trade is on display in Indonesia where transactional politics are now producing a raft of new commitments that may be funnelled through Danantara, the sovereign wealth fund established in 2024. Although commentators cannot resist the temptation to say that Danantara will be Indonesia’s “Temasek”, this is a naive analogy. It’s easy to see that Danantara is struggling with a chaotic mandate that could ultimately put Indonesia’s investment grade bond rating at risk.

No one should conclude that this is just a story about Indonesian governance. It’s also a lesson in how Asian companies have structured their bets on Indonesia’s valuable coal and nickel supplies. Whether it’s Chinese SOEs, Korean power companies, Japanese energy companies, Vietnamese and Philippine power companies, or US nuclear interests, Indonesian insiders have been eager partners in often-opaque deals with huge tail risks that could become a tax on Indonesia’s frustrated population.

Don’t forget the debt analysts

2026 will doubtless be a busy year for deals as regional portfolio reshuffling accelerates to accommodate the shifting tides. But not all the activity plays out in the daily news flow captured by equity investors who often skate by the nuance that is lurking in the debt world or in the courts. Some of the best commentary on governance issues comes from debt analysts who track how company debt is restructured and national investment messes are cleaned up.

The political checks and balances that constrain the biggest PE funds and acquisitive conglomerates and SOEs typically operate outside the traditional governance channels. As a result, it’s access to bank financing and debt markets that often proves to be the real check on viability. In the past, this has forced debt analysts and the credit rating agencies to be the reluctant guardians of the national financial plumbing. But they hate to lead on bad news.

That’s why Moody’s and Fitch’s recent decision to downgrade the outlook for Indonesia’s sovereign debt is so concerning. Moody’s did not mince words in its 5 February 2026 outlook downgrade, noting that it was "driven by reduced predictability in policymaking, which risks undermining policy effectiveness and points to weakening governance”.

Rating agency commentary like this should be a wake-up call for investors and policymakers drunk on AI dreams and simplistic assumptions about how new energy infrastructure will be funded. Political risk is rising for both politicians and company insiders who fail to appreciate that government generosity inevitably comes with strings attached. The cost to all parties can be hard to calculate. That’s the challenge of macro governance risks. But by the time the problem is evident, the money is gone and the assets are worthless.

Copyright: Ninepin Ltd, 2026