Iran, Asia, and energy transition: What have we learned so far?

A reality check on how the Iran War will impact Asian energy markets. Five themes stand out.

As we strap in for another week of chaos from the Middle East, it’s time for a reality check on how Asian markets are adapting to potentially drastic changes in global energy markets. In recent years, the sector has been driven by competing goals with energy security facing off against affordability and a pivot to cleaner energy.

The macro governance angles—how subsidies are managed, which countries hold the upper hand in supply relationships, and how technology will be financed—have always lurked in the background. But any illusion that all these market dynamics are well understood is now coming under pressure. The Iran War is giving everyone a chance to revisit their assumptions about once boring energy and power markets.

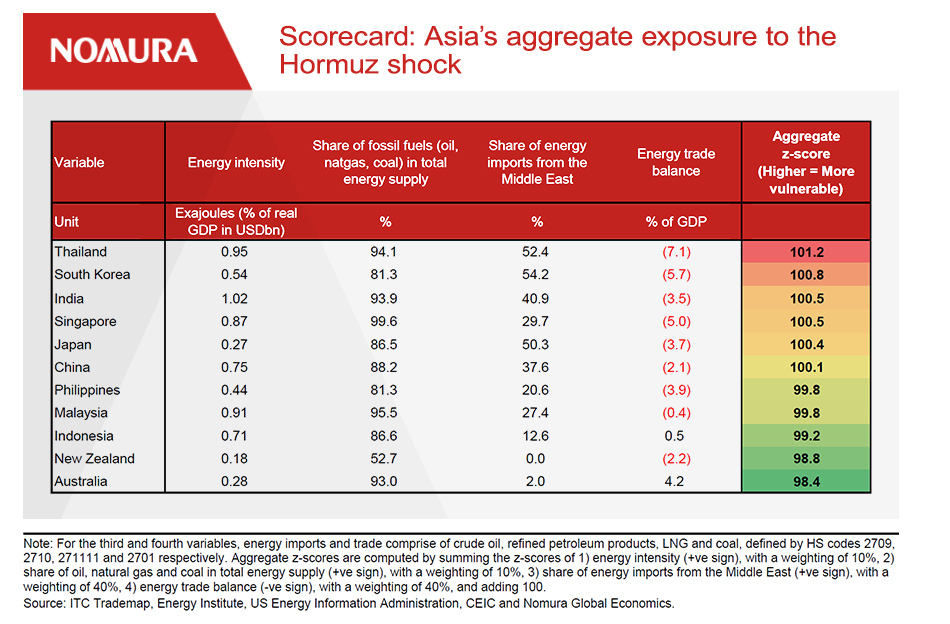

First, let’s acknowledge what is reasonably well understood. The headline winners and losers are clear under most scenarios: in North Asia, Korea and Japan face broad-based economic risks to their energy and industrial sectors, while Thailand and India face immediate supply risks that will punish the economy.

The Philippines, which just added LNG to its energy mix, is managing an old school fuel crisis and risks to remittances, Vietnam has cut fuel taxes to offset consumer impacts, and Indonesia is searching for new oil supplies to offset limited storage. China’s dependence on imported oil is a well understood risk, but Beijing is in a unique position with the resources to manage its vulnerabilities and to benefit from its technology dominance in renewables.

Source: Nomura (https://www.nomuraconnects.com/focused-thinking-posts/asia-economic-monthly-asias-hormuz-exposure-scorecard/)

But the shock waves have already gone much further than these first-order economic effects and some valuable insights deserve more attention than they’re getting. It’s important to start tuning in now to some of these trends. The share price performance of Asia’s leading power utilities doesn’t tell the full story. Much of the action is playing out behind closed doors as government leaders look for new alliances, policymakers look for quick fixes, and bankers re-assess balance sheet risks.

What’s driving them? The following themes standout:

There isn’t an “Asian” narrative

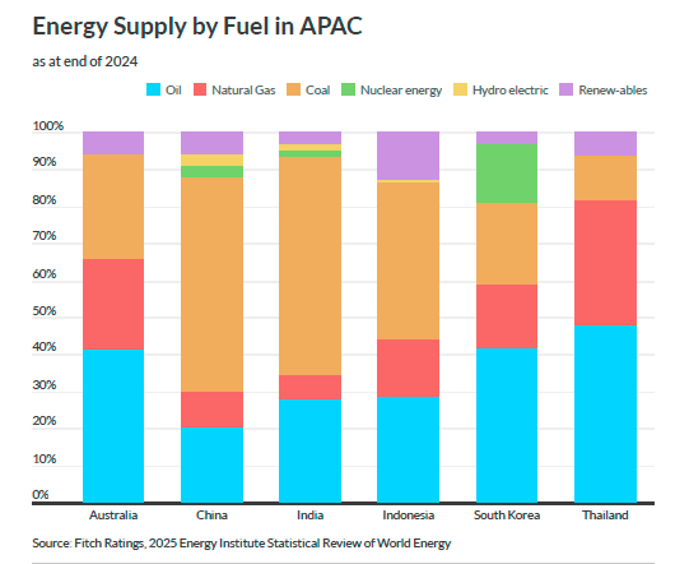

It’s only natural that strategists have tried to simplify Asia’s Iran energy dilemma. That said, any analysis of Asia’s response to the looming shortage of Middle East oil and gas must start with each country’s dependencies—and an acknowledgement of how diverse the scenario is at the country level. It’s not just about the volumes either. The impact reflects the options each country has, what domestic energy resources (coal, gas, or hydro) can be exploited economically, and what the generation mix looks like for the power sector.

One chart cannot tell the full story, but if imports of oil or natural gas dominate a country’s fuel and power mix, as they do in Thailand, South Korea, and Australia, the consequences of inaction are very high. That’s why Australian politicians are already locked in conflict about new energy policies, the Thai government has negotiated directly with Iran for safe passage for Thai oil tankers, and LNG-dependent Korean and Japanese energy officials are collaborating to stave off market disruptions.

Beware of clean energy cheerleading

Make no mistake, the strategic benefits of renewables will be an extremely valuable part of the response to the Iran crisis in some countries but the clean energy versus fossil fuel dichotomy isn’t predictive of outcomes, especially not over the next twelve months. It’s part of the story, but the role that a higher mix of renewables can play in any country’s generation mix depends on system design and financing options.

Just as there isn’t an overarching Asian narrative, there isn’t a one-size-fits technology narrative either. Keep an eye on countries like Vietnam and the Philippines where incremental additions of modular renewables along with storage can boost system capacity quickly. De-bottlenecking transmission systems and encouraging demand response should also be a priority in well managed systems.

But big decisions about future generation mix rest on a highly politicised menu of issues. The US is pushing hard to grow its market for LNG exports in Asia and to encourage more nuclear. Watch policymakers handle these trade-offs carefully along with decisions about more offshore wind and geothermal. None of this will be a quick fix, but no one will want to make enemies right now by closing off technology options.

Watch the clock, especially for nuclear

Perhaps the biggest mistake that non-power sector commentators make is to embrace bold predictions about how quickly countries can reshuffle the deck for power generation. For the past year, optimism about the return of nuclear to power AI data centers has proliferated. Some of this may happen in Asia, but it won’t happen overnight. Japan, Korea, and Taiwan have long nuclear track records and are leaning in the direction of repowering old nuclear plants and planning new ones. Indonesia and Vietnam are also open to carving out space in their energy mix for nuclear as part of efforts to pacify US trade negotiators.

For Japan and Korea, a nuclear resurgence is all about business. Mitsubishi, Hitachi, Toshiba, KEPCO, and Doosan Enerbility all hope to gain from this trend. China’s CGN and SPIC could also benefit. But never lose sight of the fact that it takes years to site, construct, test, and bring online a new nuclear facility and that’s before you address waste storage.

The key takeaway is that nuclear is never a quick fix. Development timelines are typically in the 6-8 year range for countries with a nuclear track record. And despite the breathless optimism about small modular reactor (SMR) technology, this technology is years away from reliable cost-effective deployment. The SMR “plug-and-play” mantra ignores supply chain realities. This is an industry that has none of the scale economies of solar panels or batteries.

It’s never just about fuel

Over the past year, the Trump Administration has returned to its war against offshore wind and renewables to benefit US gas domestically and LNG exports globally. This is a pivot that the Japanese and Koreans have happily embraced. In Asia, they have worked hard to keep the gas-as-a-transition-fuel value proposition alive. Given their global investments in the gas value chain, this should not come as a surprise to investors.

What’s less well understood is how misleading it is for policymakers and industry advocates to describe decisions about LNG imports as a simple choice about the cost of LNG as a fuel. The is especially true if it’s framed as a choice about long-term power system design.

It’s fair for power system operators to want some of the characteristics of combined cycle gas in a responsive power system with a mix of firm and variable power sources. But it’s distinctly inappropriate to hide the fact that making a long-term commitment to LNG involves huge investments in a gas value chain, including storage, pipelines, and the patience to join a long queue of buyers waiting years for a new gas turbine.

Economic policymakers must also consider the foreign exchange and energy security risks associated with sourcing LNG from the Middle East, the US, or the international traders now clustered in Singapore. Moving time-sensitive cargoes through the Strait of Hormuz or the South China Sea in periods of heightened geo-political risk is a bad fit for countries that lack a blue-water navy.

And don’t lose sight of the role that Japan, in particular, plays in making a market for LNG cargoes. Leading Japanese companies like JERA, Tokyo Gas, Osaka Gas, Mitsubishi, Mitsui, and INPEX are all consequential gas traders with a global footprint. Japan’s role extends well into the financial sector as well with MUFG, Mizuho, SMBC, and JBIC underwriting the industry globally.

Asian industry insiders are well aware of the scale of Japan’s role in the gas sector thanks to pressure from their Asia Zero Emission Community (AZEC) strategy to push new LNG and hydrogen projects across Southeast Asia. Progress has been slow for AZEC because project costs have continued to balloon. But headwinds on a new round of LNG-to-power deals shouldn’t be taken to mean that Asian investors can assess all the financial and policy risks involved.

Nonetheless, the red flags continue to pop up. In a revealing article last week, Nikkei Asia detailed how Vietnam and the Philippines, both import-dependent buyers of energy, have been asking the Japanese government for help in sourcing crude oil as they face impending shortages in domestic reserves. (See "Vietnam, Philippines seek oil aid from Japan amid Mideast War", Nikkei Asia, 27 March 2026)

Iceberg warning

The macro governance point to stress is simply that the financial fallout from the Iran War is going to test the market’s ability to differentiate between short-term event-driven news and the market responses that support long-term revenue growth—not just puffed-up order books. For Japan, China, and Korea, leadership will depend on their willingness to offer both technology and financing solutions for Southeast Asia. The hard part of the bet is whether these governments have the financial capacity and political will to partner with Asia’s energy growth markets without a business-as-usual safety net.

Copyright: Ninepin Ltd, 2026