Doosan Enerbility and the trouble with national champions

As Seoul bets big on nuclear power again, investors are rediscovering the complexities of strategic energy

Over the past 18 months, Doosan Enerbility’s stock has been on a roll. Just two years ago, the infrastructure and heavy equipment company was mired in controversy, and the earnings outlook was uninspiring.

Now the stock is a picks and shovels story on steroids. As Korea’s leading power equipment manufacturer, it sits at the nexus of a nuclear power renaissance both at home and overseas thanks in part to the Trump Administration’s love affair with all things nuclear and the global AI data centre power demand boom.

The stock broke out of the doldrums in early 2025 and is up 227% on a total return basis over the past year, versus 186% for the KOSPI. And despite the governance mess, it’s up 610% over the past three years and trading on a price to earnings multiple of more than 500 times trailing earnings and a price to book of 10 times. As a result, the stock is in MSCI’s Korea Index sitting alongside well-known Korean names like Hyundai Motor and KB Financial.

The question now is whether the company’s nuclear news story has legs, and whether local analysts and investors understand nuclear power sector fundamentals well enough to assess the complex implementation risks that the company faces based on aggressive forecasts for the order book.

This analytical dilemma—optimistic local analysts versus more circumspect international investors—is a common point of tension when it comes to assessing homegrown national champions. Local analysts usually have better management access if they are positive on the stock, but many also lack an understanding of Doosan Enerbility’s global peers and the competitive dynamics that set the terms for long-term investment in the global power equipment market.

This matters because the global power sector is accumulating political risk that is increasingly hard to analyse, even for the experts. For Doosan to meet optimistic expectations, a lot must go right in a world that is battling shifting political alliances, tight funding, and structural shifts as cheap renewables and the electro-state narrative chip away at the economics of LNG-fired power and high-cost first-time nuclear installations.

A bet on yet another national champion

Doosan has been considered a political insider for years despite its position outside the top tier of Korean chaebol. The company, with an estimated 30% of the shares held by the Park family, got things very wrong with their attempted restructuring involving Doosan Bobcat in 2024. But thanks to their ability to maintain government support, they were able to lean into their long history in the infrastructure and heavy equipment world to craft a dramatically refreshed growth story.

Doosan’s strong power technology portfolio with growing export potential has given the company a position at the centre of “Team Korea’s” global growth ambitions, locking in active government backing regardless of the party in power. This support is existential for Korean policymakers thanks to the company’s deep links to government-backed domestic partners. Doosan Enerbility’s ability to successfully scale its combined cycle gas turbine business and its small modular reactor (SMR) production platform is critical to KEPCO and Kogas—both of which are facing headwinds.

Government support is also needed for Doosan’s deals to reach a financial close. Most of its projects require large slabs of government-subsidized credit enhancement from KEXIM and K-Sure as well as permissive tariffing regimes at the project sponsor’s end to underwrite expensive capacity.

More, better, higher—the bull case

To appreciate the analytic challenge for investors—and Doosan Enerbility’s implementation risk—it’s crucial to appreciate the pressure on the company to deliver major projects at home and in new markets overseas. It is also expected to master demanding new technologies, scale so-called “first-of-a-kind” manufacturing facilities and implement complex projects that typically require multiple layers of regulatory approvals in new markets.

Doosan Enerbility’s core earnings outlook is driven by optimism about its large project pipeline (EPC contracts) and product sales. As a result, analysts’ forecasts for the company rely heavily on guidance from the company and a superficial treatment of the company’s order book and margin assumptions.

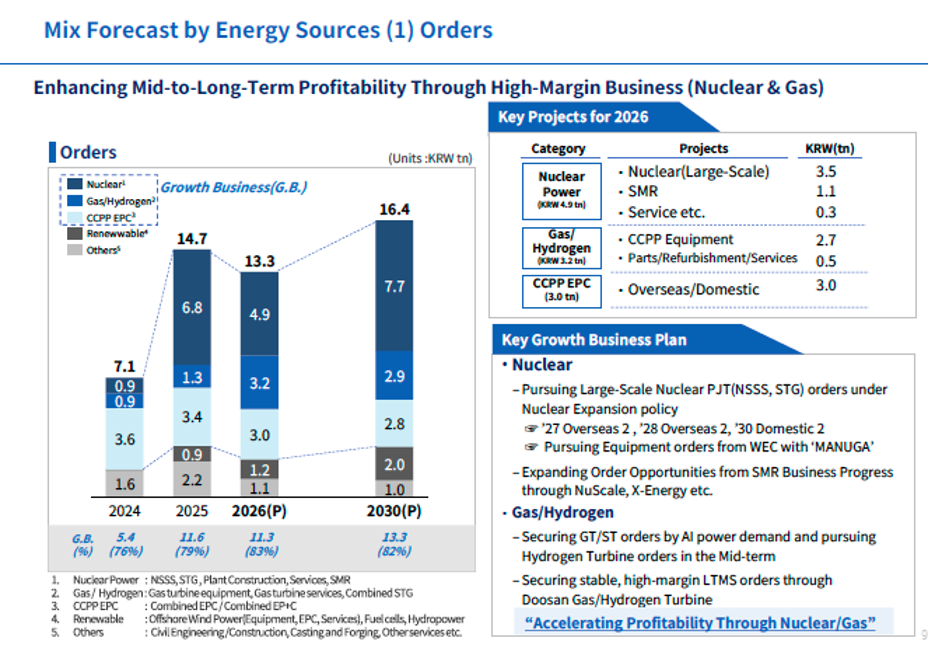

The table above maps out the company’s guidance on its order book and highlights the company’s pivot to nuclear projects and SMR equipment sales. Doosan’s nuclear growth story comes in two parts. The first is based on their track record with large scale conventional nuclear reactor pressure vessels and steam generators.

The most reliable part of Doosan’s outlook stems from their role as a key supplier to KEPCO and their export track record in a handful of markets in the Middle East and Eastern Europe. The project pipeline now reflects projects scheduled for delivery out to 2040 with expected wins for their nuclear technology in newer markets like Saudi Arabia, Vietnam, Turkey, Uganda, and the Philippines. That’s a mixed blessing for forecast reliability as many projects lack firm orders and financing.

The second part of Doosan’s nuclear story is all about hopes for a rapid scale up of the market for SMRs. The excitement about SMRs reflects optimism about the ability of new small-scale nuclear reactors with modular design to meet a range of special purpose use cases in markets that need local sources of firm power. The hope is that these smaller units can deliver baseload 24/7 supply and benefit from falling cost curves that could help them compete with low-cost renewable technologies firmed with batteries.

Doosan has been energetic in chasing the SMR opportunity via its alliance with KEPCO-controlled Korea Hydro & Nuclear Power (KHNP) and has enjoyed strong backing from the government due to the potential for a leadership position that could be advantageous to Korea on the global stage. Doosan partnered with NuScale at an early stage but, as NuScale fell off the pace, they have focused on an alliance with X-energy for production of Xe-100 components at a US$540m facility being built at the company’s Changwon plant for units to be deployed in the US.

Doosan’s earnings momentum is not just from nuclear. The outlook will also benefit from sales of combined cycle gas turbines and boilers—a high-value technology where Doosan recently cracked the top tier with domestic sales of its own H-class gas technology to KEPCO. Three years ago, the company’s focus on gas turbines didn’t look like a natural winner, but the bet is coming good as AI-linked power demand has unlocked new demand that cannot be met by the incumbent suppliers.

Korean analysts have translated Doosan’s growing project pipeline into a high growth earnings scenario. Backed by the company’s guidance, one leading domestic analyst forecasting out to 2030 has penciled in orders for more than 10 new large scale nuclear projects, 40 SMR unit sales, and more than 30 gas unit sales. In 2030, progress payments and sales are then expected to balloon by more than 300% for nuclear and nearly 200% for gas units compared to 2026. Meanwhile, EBITDA margins are estimated to improve by close to 50%.

Things that could go wrong—the bear case

It’s easy to write about why this is a dream time for nuclear and how Doosan Enerbility’s high-cost effort to chase localization of combined cycle gas technology could pay off thanks to AI-driven demand. It’s harder to risk-adjust the timing and margin on any one project or a new technology like SMRs. Nonetheless, that’s what seasoned regional analysts are trained to do.

Doosan management and government backers may not welcome a conversation about every project detail, but questions about the risk profile of the company’s project pipeline are fair game. The proposed projects in Vietnam and Texas are good proxies for testing the implementation risks embedded in Doosan’s geographically diverse project pipeline.

For example, optimistic project assumptions can be tested on Ninh Thuan 1 & 2, the two projects that Doosan hopes to supply in Vietnam. Questions should be asked about Vietnam’s readiness to go all-in on large-scale nuclear without highly concessionary terms and easy financing from Korean banks. KEXIM and K-Sure will doubtless have to prioritize this project to make necessary compromises.

In the meantime, expect EVN and PVN, the domestic Vietnamese energy and power SOEs sponsoring the projects as well as hard-pressed Vietnamese regulators to monitor this project with care. None of these parties have deep expertise in overseeing nuclear projects. They will be developing capacity on the fly with little margin for error.

Four projects for Fermi America are also a part of Doosan’s nuclear pipeline via their key equipment supply partnership with Westinghouse. Fermi’s ambitious 4GW Matador project is planned for Texas and has enjoyed high profile Republican political backing. Nonetheless, Fermi is currently in crisis as initial backers and project participants have stepped back raising questions about both the company’s and the project’s viability.

Perhaps the biggest set of risks comes from Doosan’s enterprising pursuit of SMR opportunities. It is broadly understood that scaling SMR technology could take at least a decade and NuScale’s high profile project cancellation in Utah looms large as a cautionary tale about first-time technology and market risks.

For the time being, X-energy is certainly viewed as a stronger player than NuScale. With KHNP taking the lead for Team Korea, Doosan may be sheltered from some financial risks. Nonetheless market insiders will be keen to stress test X-energy’s progress very pragmatically given Doosan’s vulnerability to downside surprises if implementation risks begin to accumulate.

Once bitten, twice shy?

The challenge for investors is that Doosan Enerbility’s share price performance leaves little room for a nuanced view given its checkered history of delivering earnings on its global project portfolio. After the Doosan Bobcat mess, large investors should be at least a little cautious about suspending disbelief. The stock has delivered, but management has not yet earned full trust.

This is the time for global investors to ask more astute questions about project risks and to risk-adjust consensus forecasts. Also cast an eye over Doosan Enerbility’s board. It has a slate of well-credentialed senior Korean professionals with inside credentials. But none of them have a track record in the global power technology market. Independent control of the audit committee is a good thing, but it’s hard to feel confident that this is a group that can form its own view of global power market trends.

We are also left to wonder what Doosan Enerbility thinks about the macro governance risks that can derail even the biggest global heavy equipment companies when power sector norms and political alliances shift. If Doosan is going to chase US projects which rest on the political backing of the Trump Administration, it’s important to consider what might go wrong. That’s also true in Vietnam which has been content to play a long game on power sector development.

It’s time for Doosan Enerbility investors to ask more of the company and of analysts. These governance risks are material, but you have to ask better questions.

Copyright of Ninepin Limited, 2026